- Home

- Markets

- Who We Are

- Mission

- Services

- Newsletters

- Livestock Sales/Services/Sources

- Ag Links

- Contact Us

- Livestock Overview

- Market Overview

- Futures

- Options

- Charts

- Historical Data

- Market Heat Maps

- AgPlus

- Cash Bids By Zip

This Underdog AI Stock Is Up 380% in the Past 6 Months. Analysts Think It Can Still Gain 70% From Here.

/AI%20(artificial%20intelligence)/AI%20technology%20-%20by%20Wanan%20Yossingkum%20via%20iStock.jpg)

Rezolve AI (RZLV) is a London, UK-based tech firm that deals with AI-driven commerce infrastructure, allowing companies to deploy shopping, pay, and even fulfillment agents that work autonomously using its Brain Suite platform. The company exists within the go-grow enterprise artificial intelligence (AI) commerce market, teaming up with names like Microsoft (MSFT), Alphabet (GOOG) (GOOGL), and even Tether (USDTUSD). Rezolve presently has a market cap of a little over $1.3 billion, which makes it a mid-cap growth stock within the AI-commerce realm.

In the last 52 weeks, RZLV shares have ranged between $1.07 and $8.45, recently trading around $6.20, showing a one-week rise of 24% and a swift recovery from year-earlier lows. The stock’s increase comes after management lifted revenue guidance and showed robust momentum on a company enterprise pipeline. Although Rezolve lags the overall Nasdaq Composite ($NASX), its recent pickup presages a return of institutional attention after several months of consolidation.

Valuation continues to be speculative given Rezolve's accelerated scale. The firm currently experiences negative earnings with a negative profit margin, an approximately 6,959x price-sales (P/S) ratio, and a -0.74 debt-equity (D/E) ratio, a reflection of early-stage risk and dilution risk. Gross margins of 95.8% and increasing recurring revenue bode, nonetheless, for quick improvement in operating leverage when growth expenses normalize. Rezolve does not pay dividends; rather, it continues reinvesting for market share capture.

Rezolve AI Matches Expectations and Raises ARR Targets

Rezolve's first-half 2025 results easily beat Wall Street expectations. Revenue jumped 426% year-over-year (YoY) to $6.3 million, beating consensus $5.1 million estimates. Adjusted EBITDA at $17.7 million modestly beat the forecast $18.7 million loss, revealing better cost management despite phenomenal growth.

The ringer was yearly recurring revenue. Rezolve reported over $90 million ARR year-to-date (YTD) and lifted full-year guidance to at least $150 million ARR exit rate for the year 2025—up significantly above earlier internal projections. Forward, management set a lofty 2026 ARR guidance of $500 million, attributing much of it to “strong demand momentum and visibility into its customer pipeline.”

Enterprise adoption stepped up further. More than 100 worldwide customers now deploy Rezolve’s Brain Suite—among them H&M, Ferrero, Rakuten Group (RKUNY), Office Depot (ODP), Urban Outfitters (URBN), and Mango.

The platform’s “Agentic Commerce” features deliver autonomous AI agents that search, transact, and personalize in real time, a defining next-generation retail tech differentiator. Professional-services partners such as Cognizant, PwC, and Wipro assist in deploying Rezolve’s systems at scale, expanding its reach further.

CEO Daniel M. Wagner noted that “Brainpowa,” Rezolve’s proprietary technology that resulted, was at benchmark level with GPT-4 and Claude while having virtually zero hallucinations—putting the company on the map as an enterprise-class solution for commerce-enabled AI. At gross margins close to 96% and contracted ARR for the majority of 2025, Rezolve is structurally well-positioned for a pivot from concept to cash-flow traction during the next 12–18 months.

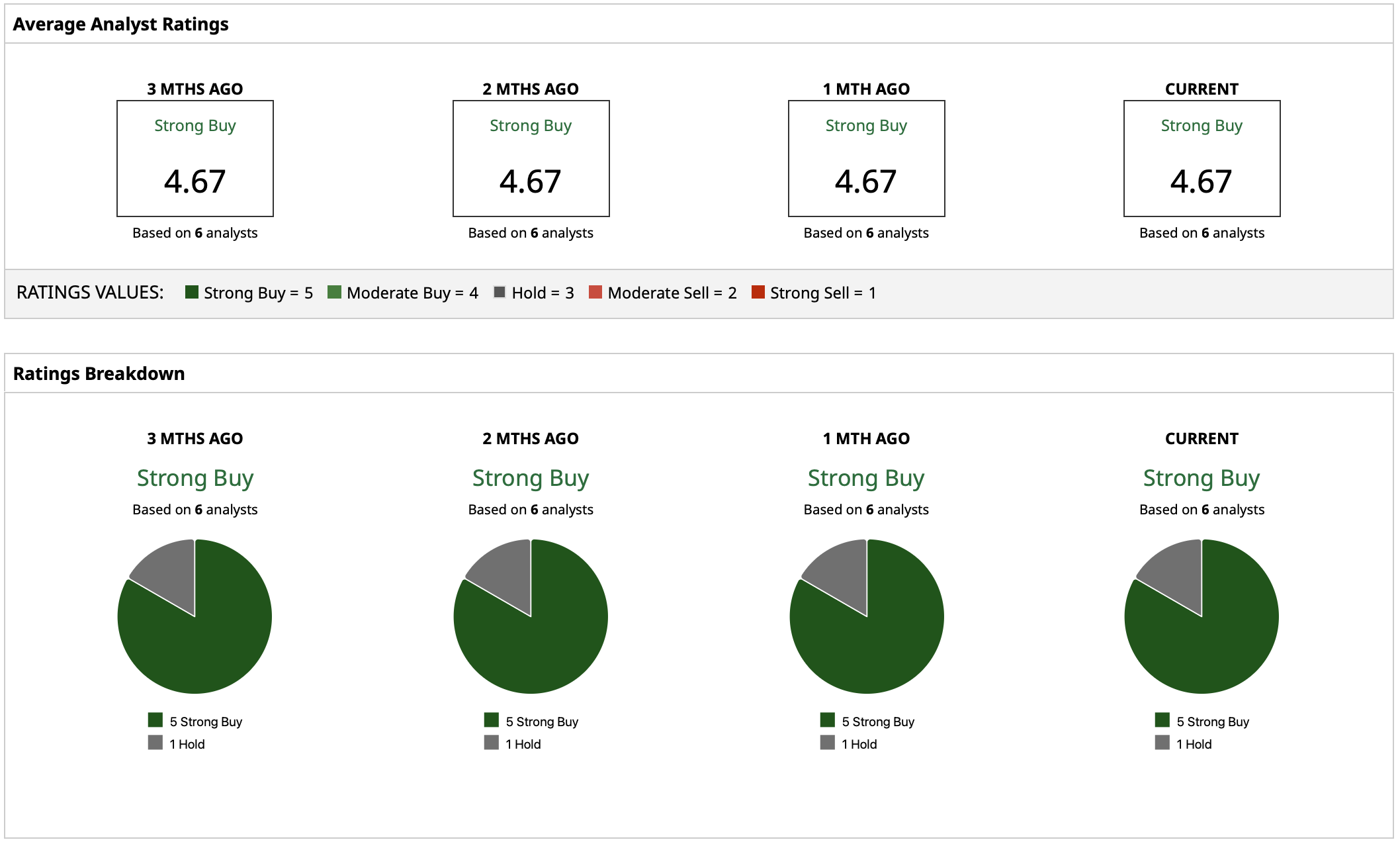

What Do Analysts Expect for RZLV Stock?

RZLV has a “Strong Buy” rating consensus with target prices set between $7 and $15, with a median target of $10.42. Based on its current price of about 6.20, that suggests potential gains of nearly 70%. The high-end target of $15 suggests over 140% upside, a clear indication that there is confidence Rezolve’s trend bodes well for sustained re-rating should execution remain the case.

Although volatility is elevated considering first-phase fundamentals, sentiment from analysts has shifted significantly bullish after the company raised its ARR guidance and growing enterprise partnerships. Ongoing demonstration of contract conversions along with margin scalability will remain integral catalysts for any sustained upside here after.

On the date of publication, Yiannis Zourmpanos did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.